Divorce, similar to death or taxes, may not be a popular talking point, but when you are faced with this reality, it is worth understanding what is involved in relation to your pension entitlements.

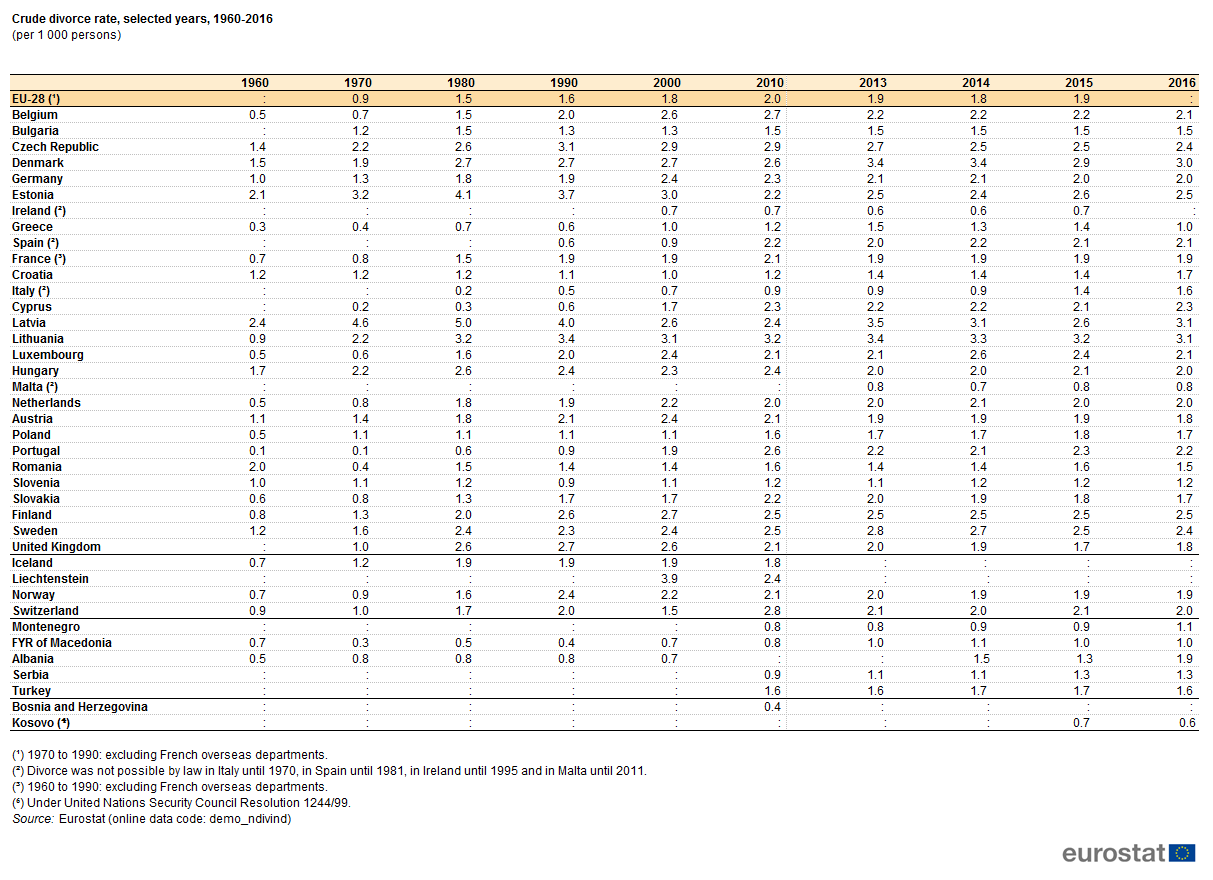

In 1995, the Irish public voted to legalise divorce. A year later, it was written into law. While the rates of divorce have been increasing in recent years, we still have one of the lowest rates of divorce in the world. The crude divorce rate in Ireland is 0.6% a year for every 1,000 people, compared with 1.9% for the UK and 3.2% for the US*.

Why Your Divorce Will End Up in Court

Did you know that after the family home, a pension is often the most valuable asset a separating couple have? The Family Law Act 1995 and the Family Law (Divorce) Act 1996 enable Courts to share out pension rights between separating and divorcing couples.

Regardless of how amicable a separation, pension rights can only be divided by a Court Order. This system can sometimes be seen as complicated. As a result, couples opt to focus on the other assets and leave the pension alone, thereby negating the need for Court intervention. A spouse, a civil partner or a qualified cohabitant (subject to meeting certain conditions) can apply for a Pension Adjustment Order “PAO” at the end of a relationship. For the purposes of this article, I will refer to spouse but the information also applies to civil partners and qualified cohabitants.

Divorce and Pensions – The Process

At the beginning of the process, each spouse is required to give particulars of his/her property and income to the other spouse and this information will include full detail in relation to a member’s benefit under a pension scheme.

After consideration of this information, the Court may serve an order (known as a pension adjustment order or PAO), on the Trustees of the pension scheme of which either spouse is a member. This PAO can require the Trustees to pay a portion of the pension benefits to the other spouse or for the benefit of a dependent member of the family. The PAO requires that the Trustees pay a specified part of the retirement benefits or contingent benefits to the person(s) named in the order.

PAOS May be Made in Respect of the Following Pension Arrangements:

- Occupational Pension Schemes, in relation to retirement benefits and any contingent benefits (i.e., benefits payable on death in service). This can apply to a current pension scheme or a pension scheme of which you were formally a member.

- Additional Voluntary Contributions (AVCs).

- Personal Retirement Savings Accounts (PRSAs).

- Retirement Annuity Contracts (RACs) including Trust RACs.

- Buy out Bonds/Personal Retirement Bonds.

It is important to note that a separate PAO is required for each separate pension arrangement in your name. In addition, benefits payable under the Social Welfare Acts and disability benefits arising under an Income Protection policy are not considered pension benefits in the context of the legislation.

Divorce and Pensions – Your Options

Following the making of the PAO, the pension scheme Trustees will notify the person in whose favour the order is made. The Trustees will inform the person the amount and nature of the retirement benefits and/or contingent benefits designated under the order.

How Benefits are Calculated?

Firstly, the Court will rule on two key factors determining the amount. These are the “relevant period” and the “relevant percentage”. The relevant period may refer to the period of and can not be later than the date of granting the decree of judicial separation or divorce. This means future benefits can not be shared.

This information will also include the option of a transfer value that may be available in lieu of keeping the benefit under the existing pension scheme. For example, a PAO may be outlined as follows:

- The period of reckonable service over which the designated benefit is deemed to have accrued, is the period commencing on 1st January 2005 and ending on 1st January 2015.

- The relevant percentage of the Retirement Benefits accrued over the Designated Period and to be paid to the Beneficiary is 50%.

In the example shown, the spouse (who is not a member of the pension scheme), will get 50% of the benefit which the member earned in the ten year period shown. The formula for calculating the benefit due will differ depending on whether the pension scheme is defined benefit or defined contribution. In either case, the spouse who has been awarded the PAO will be offered a transfer value. They may also be given the option of establishing an independent benefit within the member’s pension scheme.

Considering Remarriage?

There are some considerations when remarrying. These are:

- The Court will not make a PAO if the spouse who applies for it has remarried.

- If a PAO in relation to retirement benefits is made, this will be unaffected by a subsequent change in marital status of either spouse.

- A PAO in relation to contingent benefits (benefits payable on death in service) cease to have effect if the spouse who is not a member remarries.

Impact of a Member Retirement on the Spouse

If the member spouse retires and the spouse who benefited from a PAO has not transferred their benefit to another pension arrangement or has not established an independent benefit, the non-member spouse must also retire. A PAO must also be considered at retirement in relation to Standard Fund Thresholds and Tax Free Lump Sum payments.

Standard Fund Thresholds: When calculating a member’s threshold limit (currently €2 million), the member’s entitlement is calculated as the total value they would have received if a PAO was never made. If this calculation puts the member over the Threshold, the chargeable excess tax liability is divided between the member and the non-member spouse on a pro-rata basis.

Tax free lump sum: Subject to Revenue regulations, there are formulas for calculating the lump payable to a member on retirement. Currently, up to €200,000 of this lump sum can be paid tax free. Where a PAO exists, there is a separate €200,000 limit for the member spouse and the non-member spouse.

Divorce – A Conclusion

Pensions and divorce can be complex. The outline above offers some brief pointers but every situation is different. It is important that all parties involved are fully aware of all the various conditions and details involved. The Pensions Authority** have information on their website, offering a 46 page “brief” guide to the pension provisions of the Family Law Acts. In the event of an imminent separation or divorce, it is important to seek independent financial advice, in addition to legal expertise.

If you are going through a separation or divorce, our team can help. Simply send us an email (info@cpas.ie) we will be in touch. For financial advice, we recommend the financial consultants in Milestone Advisory DAC. The team in Milestone Advisory offer financial advice with a focus on the construction and related sectors.

Planning for the Future

As in life, there are many variables and changes. Planning for retirement and protecting your financial future involves forming expectations about income and expenses over the rest of your life, based on present assumptions. As the pension administrator for pension schemes in the construction industry, we have a range of solutions to help you prepare and protect your future investments. Whether you are self-employed, running a large company with multiple staff requirements, looking for life and income protection, we can help.

For more information and to find the right solution for you, contact our team for a no obligation discussion. Our team of financial specialists will put you in touch with the right team member. No obligations, no hidden fees, no jargon – just a straight forward chat to help you secure your present and your future.

Contact us via email (info@cpas.ie) or by phone (01) 223 4949

{kind=link}